This week, developers were eager to inform shareholders and anyone who would listen that they had made up some lost ground in 2024, while prime central London property prices decreased, along with the long-term profit accrued from years of ownership. House prices continued to slowly recover while rents alongside interest rates climbed. Meanwhile the Renters’ Rights Bill took another step forward, receiving its third reading in Parliament, during which further amendments were made. Welcome to another UK Property News Recap – 17.01.2025.

Past property acquisitions yielded smaller returns in 2024 compared with 2023.

Stubborn rates and economic uncertainty ate into the average gross profit on sales in England and Wales, which fell by 11% from £102,640 in 2023 to £91,820 in 2024, according to estate agent Hamptons. In London, the average seller lost an additional £32,000 in 2024 compared to 2023 levels, resulting in a gain of £172,350 last year. Despite this, 91% of households in England and Wales were found to have sold their homes for a profit in 2024, with nearly a third making six-figure gains.

Prime Central Markets take a beating in 2024

Estate agency Knight Frank found increased rates and taxation on the wealthy resulted in a lack of confidence in prime central London prices which fell 1% last year but increased 1.5% in prime outer London. Nevertheless there was a slight uptick in transaction volumes, largely generated in the second half of the year, reflecting a 0.5% rise compared to 2023 levels, when rates marginally retracted before thinking better of it post-budget.

Moving forward, inflation and deficit uncertainty will continue to stifle house price growth. As a result, cash buyers will seek out opportunities while borrowers will need a deal. Not easy in a market fraught with egos.

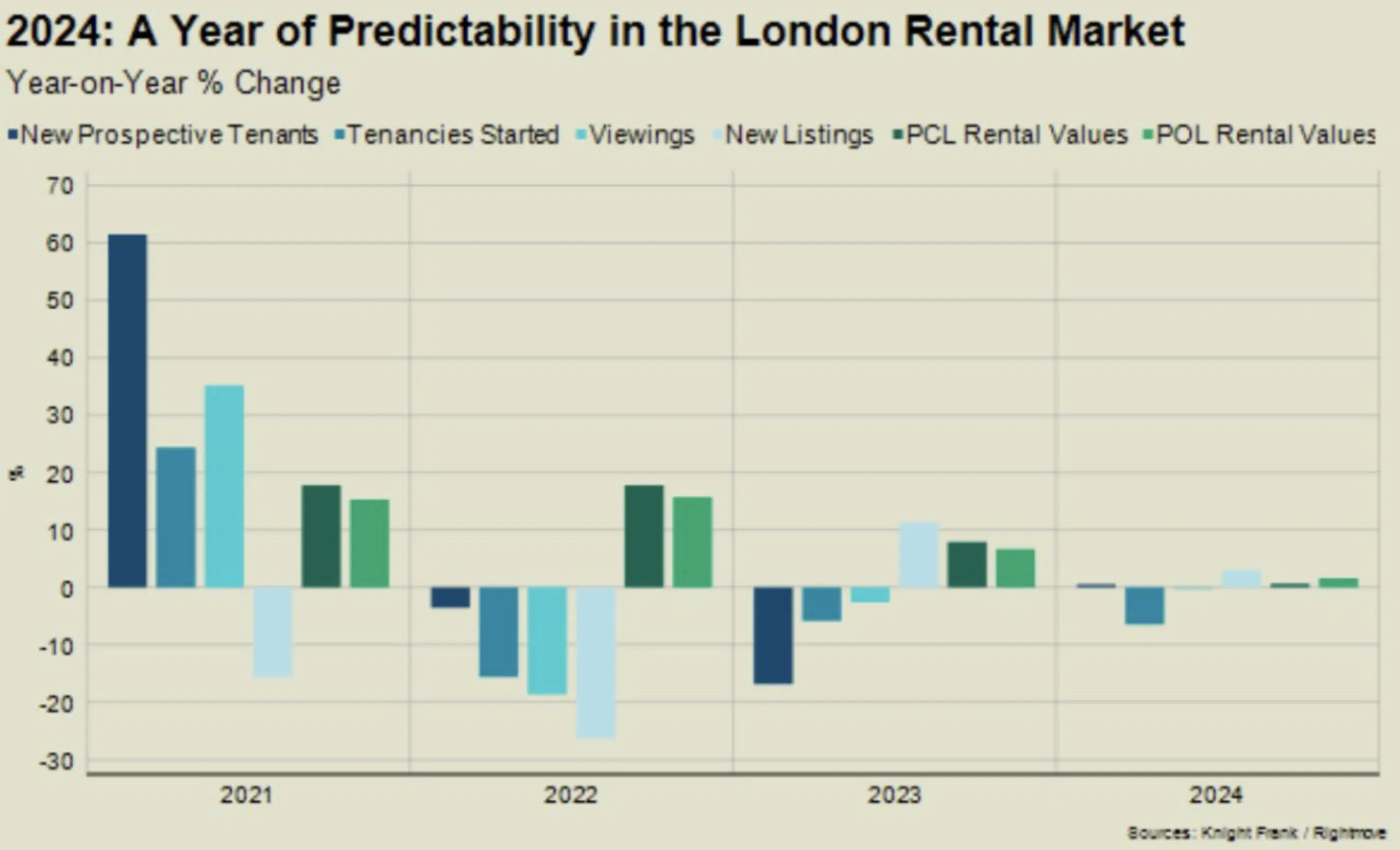

In comparison to 2023, the prime rental market saw a slight increase in prospective tenants of 0.6%, but agreed tenancies dipped by 6% despite the number of listings increasing by 3%, likely due to those unable to sell. Moving forward, expectations are for moderate to stagnant growth until there is more certainty regarding the country’s economic outlook.k.

Mortgage rates about-turn…again

In response to the recent UK economic shitshow, markets, unsurprisingly got spooked. In response, interest rates started to creep back up again.

On Monday, Moneyfact reported the average two-year fixed residential mortgage rate was 5.48% on Friday it had increased to 5.52% and the average 5-year fixed residential mortgage went from 5.26% to 5.30%.

The average buy-to-let mortgage for a 2-year mortgage went from 5.35% to 5.42% and from 5.45% to 5.55%% for a 5 year deal.

This swing in opposite directions is the result of depleted demand by unmotivated investors versus residential desperation.

Developers provide trading updates ahead of their end of year results

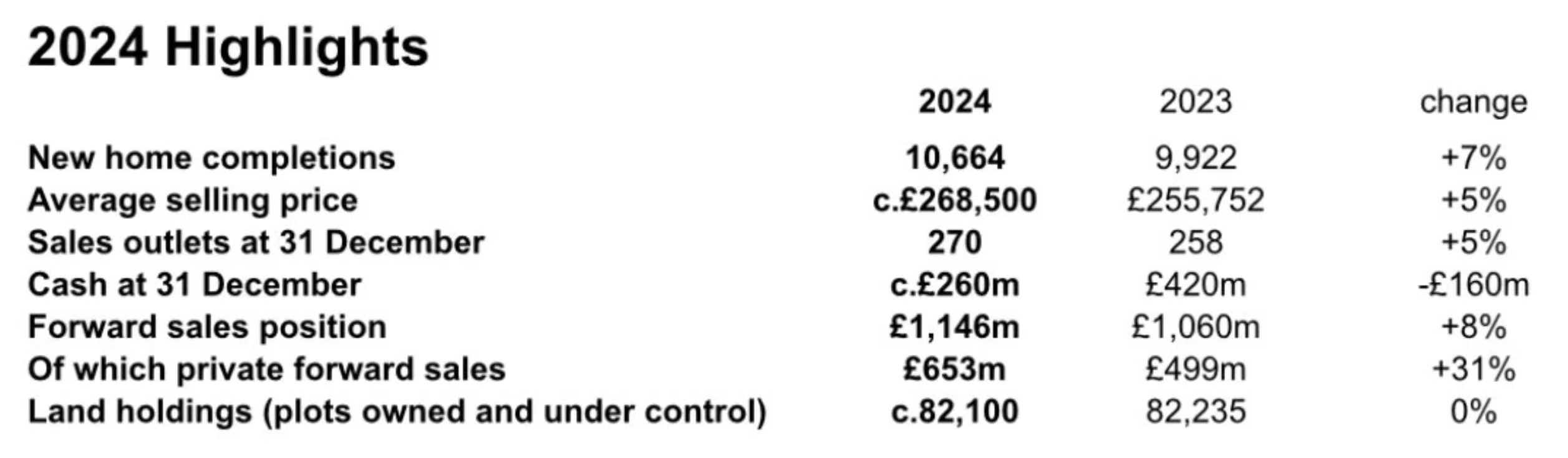

As market conditions improved, so did Persimmon’s numbers. Completions were up 7% year-on-year and despite incentives continuing to run at c.4-5% their blended average selling price (across all their brands) increased by 5% to c.£268,500 from £255,752 in 2023. Given this they expect their underlying profit before tax for 2024 to be at the highest end of market expectations; £349m to £390m.

With an 8% increase in forward sales, the group starts 2025 with confidence but remains “mindful of evolving macroeconomic and geopolitical uncertainties, including the timing of future interest rate changes.”

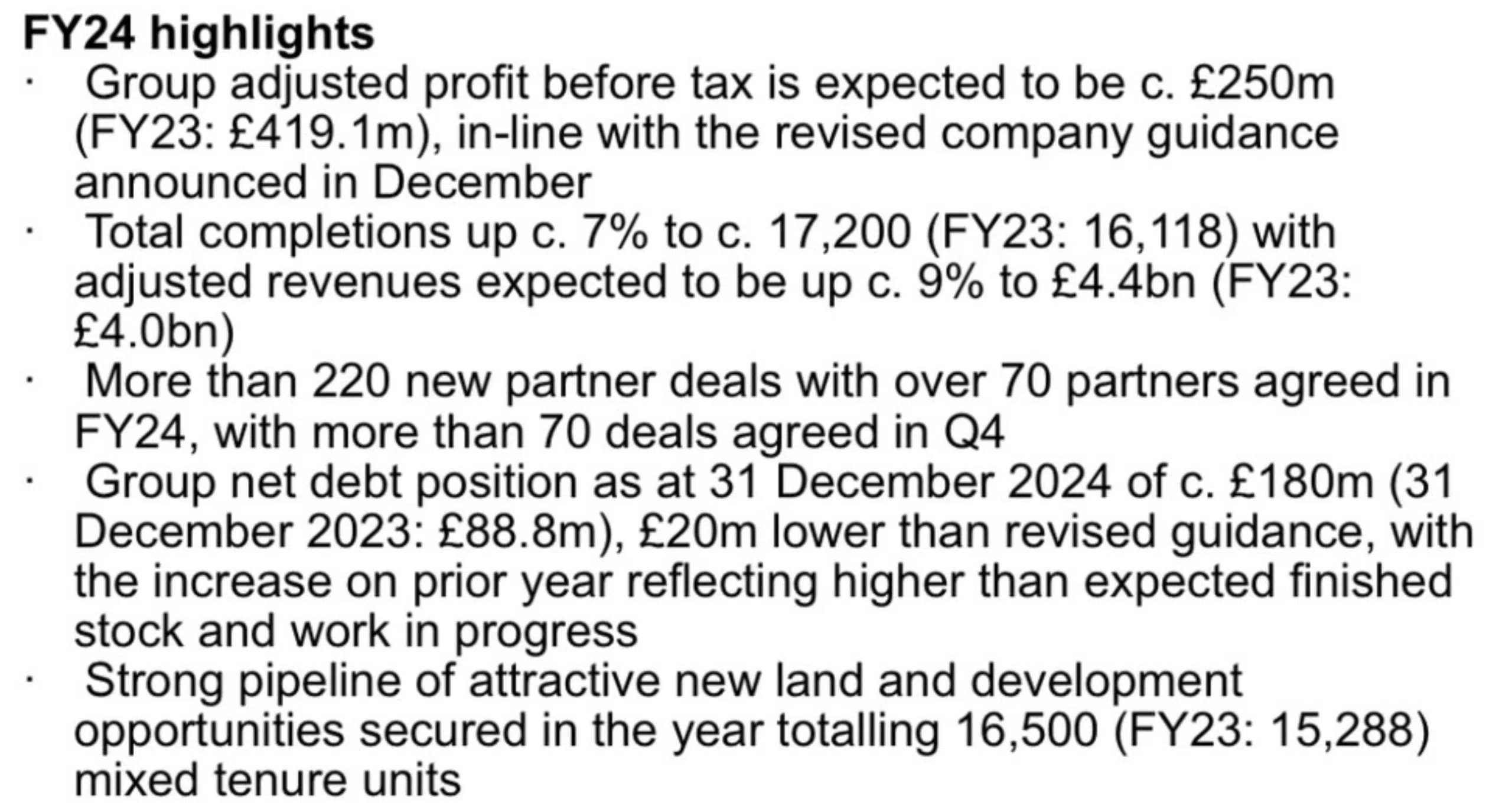

The Vistry group provided improved numbers but the difference between adjusted profit before tax in 2023 of £419.1m to c. £250m in 2024 must sting. Their sinking southern division now under new leadership and partnership completions set to finalise this year instead of last as well as new ones in the pipeline, should steady the ship and plug their net debt position further.

Taylor Wimpey also reported that completed sales were towards the top of previous guidance at 9,972, although this represents a 4% decline compared to 2023 levels. However, the group’s average selling price for UK private completions took a hit, decreasing from £370,000 in 2023 to £356,000 in 2024. Despite this, reservations increased, and approved planning for plots rose from approximately 3,000 to around 12,000.

Moving forward, increased building and employment costs are expected as National Insurance rises are implemented, which will eat into budgets and potentially affect prices.

Councils plunder second homeowners’ or investors’ coffers, in an attempt to plug deficits

Some councils are back-dating a 200pc empty home council tax premium on properties that were previously empty, but technically habitable, for more than 2 years, regardless of whether the property has changed hands. Leaving new owners to inherit bills for a property they didn’t own at the time. The question of whether a property is “habitable” would appear to extend to rats in some cases.

Average house prices continue to edge up

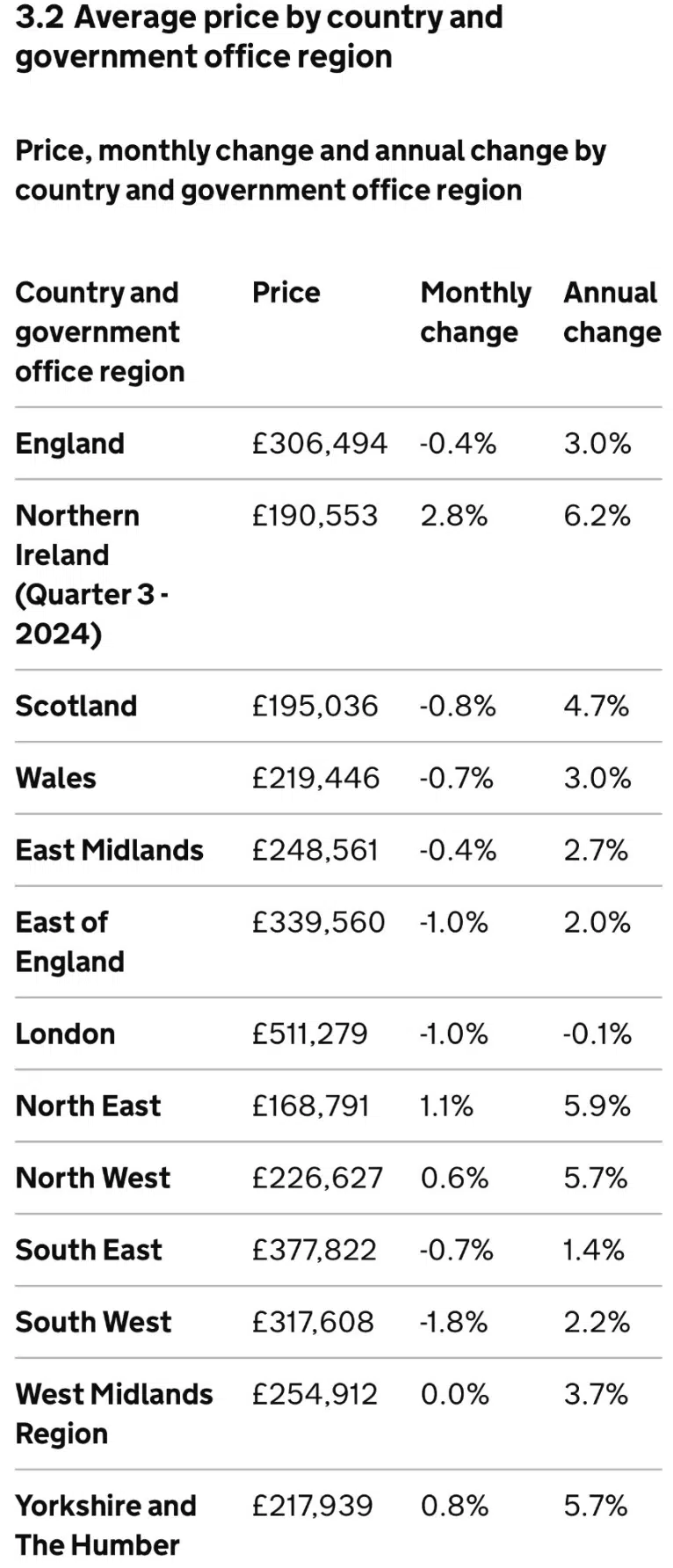

Annually, average UK house prices increased by 3.3%, to £290,000, in the 12 months to November 2024 but dipped -0.4% on the previous month.

Over the course of the year to November 2024, average house prices in England increased 3% to £306,000, in Wales 3% to £219,000 and in Scotland, they rose 4.7% to £195,000.

The biggest price growth came from terraced houses, which saw an increase of 4.7%, while the weakest growth was from detached houses, at 1.5%. Buyers remain unable to stretch to 2022 peaks but prices are clawing their way back and forth with each interest rate move.

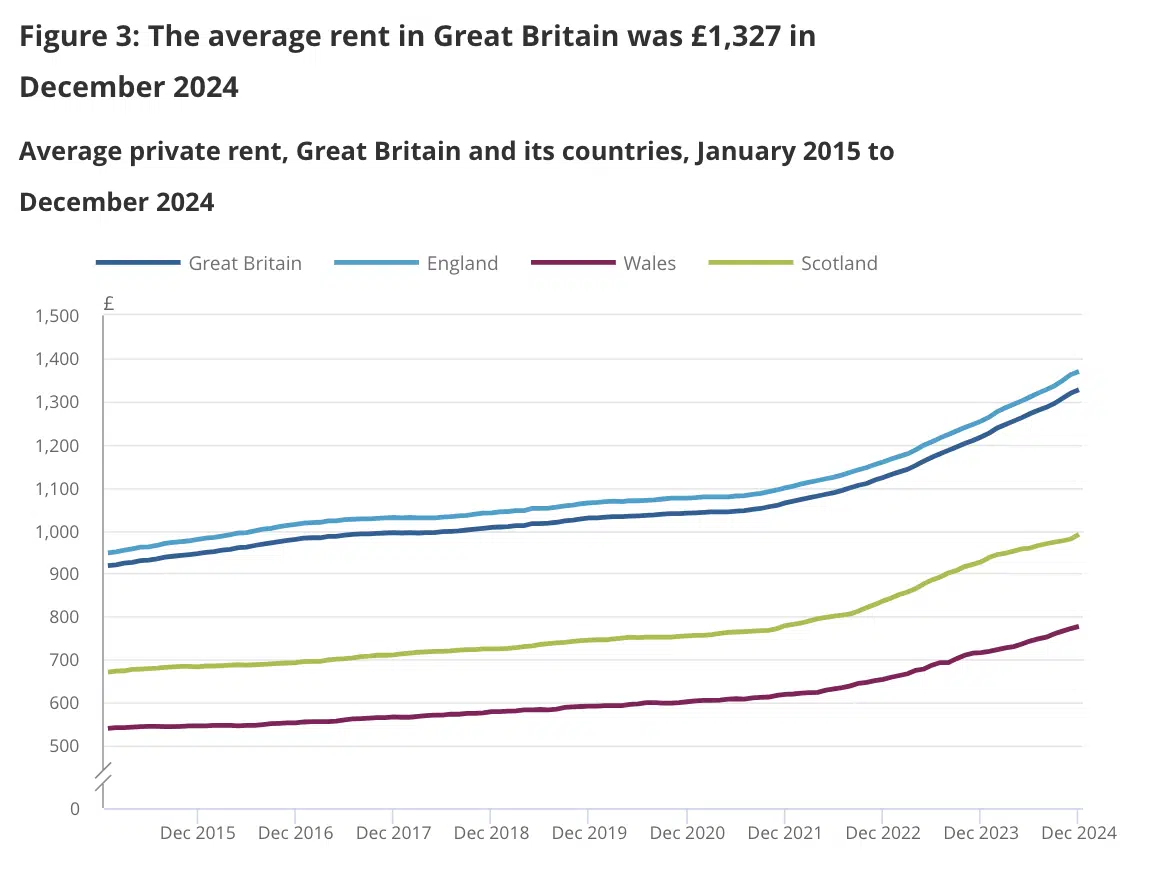

Average rents continue to rise

Average private rents in Great Britain continued to edge up, albeit at a slower rate. In December 2024 the average rent was £1,327 per month, 9.1% higher than 12 months previously.

- In England the average rent increased 9.2% to £1,369 in December 2024.

- In Wales prices rose 8.5% to £777 in December 2024.

- In Northern Ireland data currently available up to October 2024 showed average rent in Northern Ireland increased by 8.6%.

Meanwhile, average rent for Scotland was £991 in December 2024, up 6.9% from a year earlier. This was the first increase in Scotland’s annual inflation rate after 10 months of slowing annual inflation.

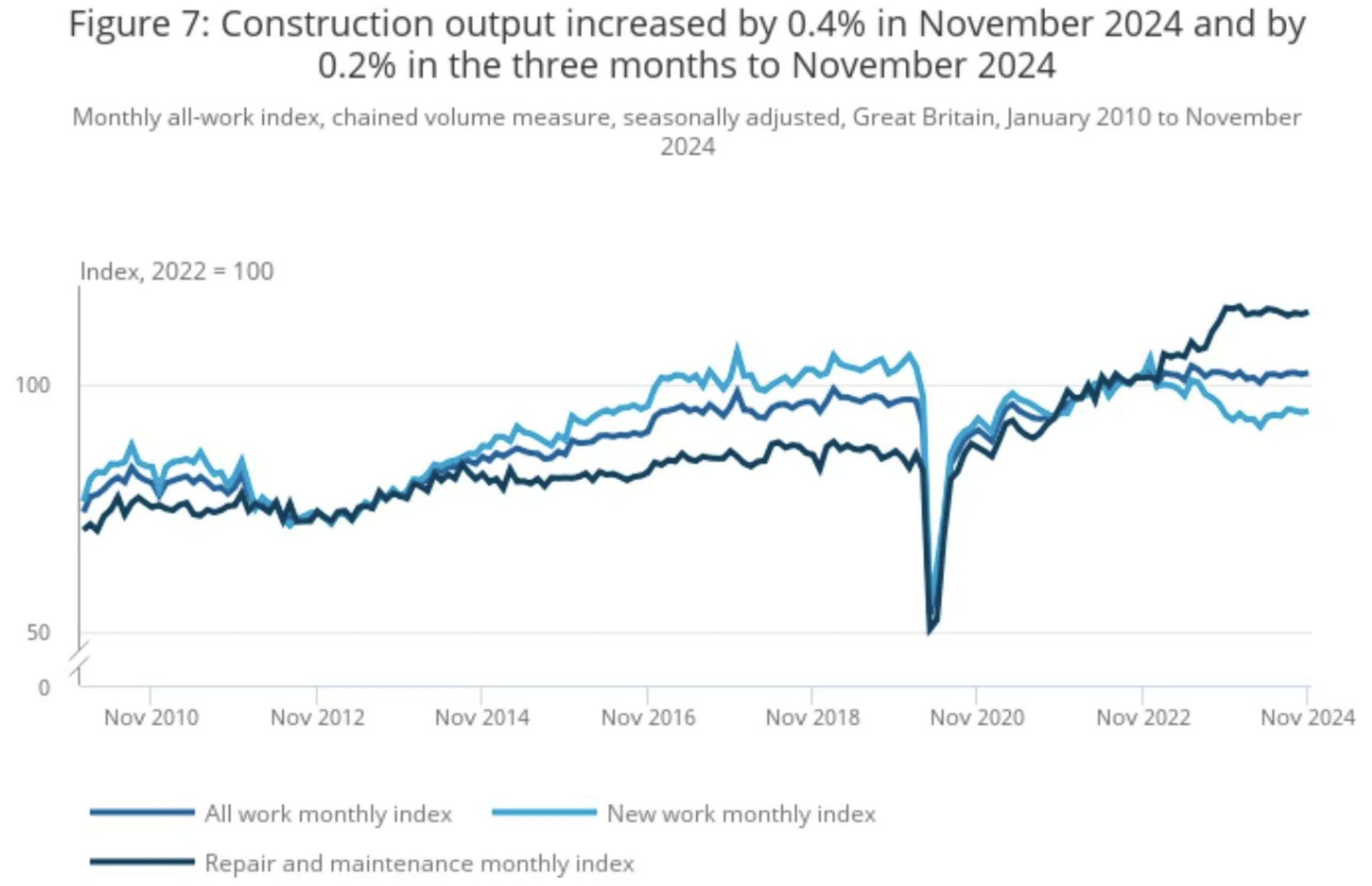

UK Construction Output – November 2024

Private industrial new work and public housing repair and maintenance provided a monthly boost to construction growth, which is estimated to have increased 0.4% in volume terms in November 2024.

The largest growth suppressant came from domestic housing repair and maintenance, which fell by 1.3%.

I expect homeowners were reining in spending in the lead up to Christmas so they have enough funds to enjoy it.

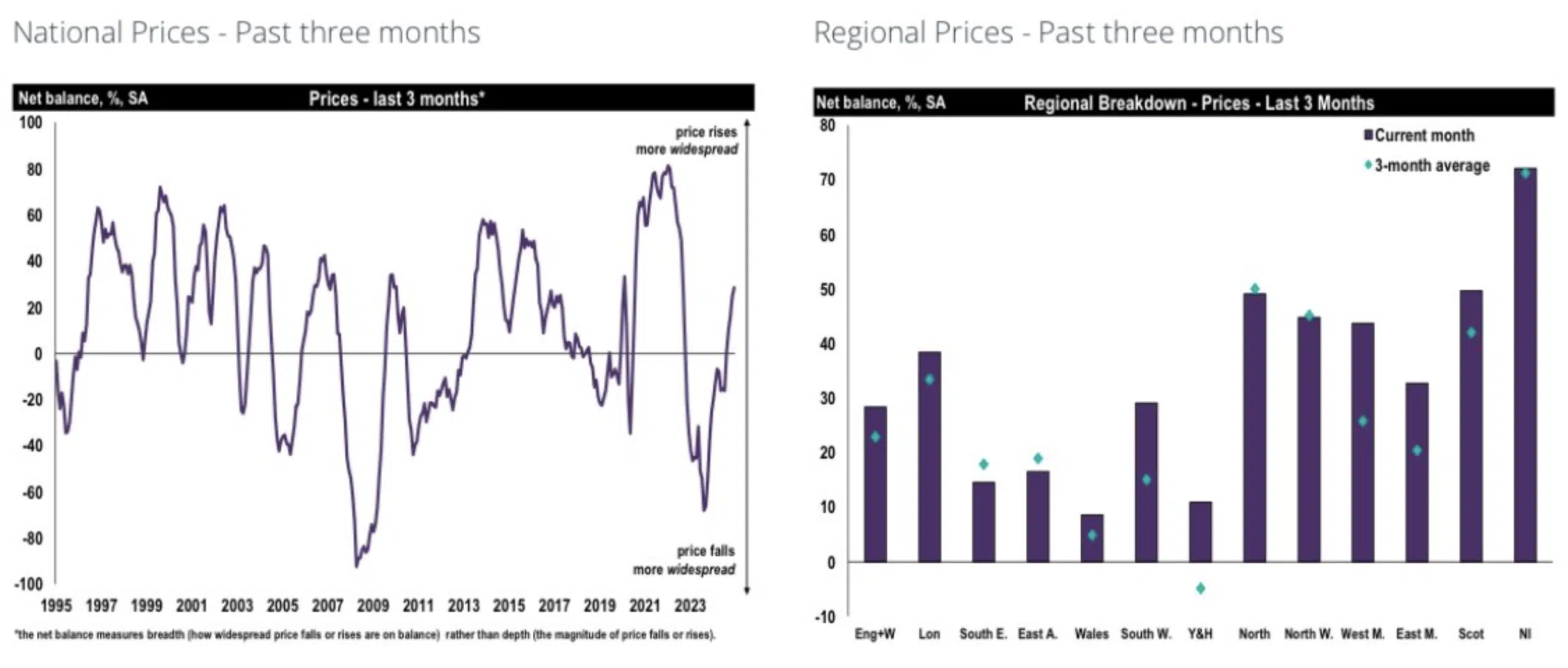

RICS residential market survey – December 2024

RICS residential market survey showed buyer demand weakened in December 2024, compared to the more positive readings in October and November, but agreed sales increased along with stock levels. Some sellers will have been hoping to attract first-time buyers keen to complete before the stamp duty increase.

At the same time, valuations soured, with some onward sellers opting to enjoy Christmas and wait for further rate movement in 2025 before listing.

As for house prices, surveyors reported growth in all regions and expect this trend to continue throughout the year, though in fits and starts, depending on when rate cuts are delivered and post stamp duty increase fallout.

In the lettings market, demand fell along with stock levels. As a result, those looking to renew or are being moved on in Spring, will have less choice and higher prices to pay.

Citigroup’s build cost stack up

Citigroup opted to be more sustainable and not knock down its historic tower block in Canary Wharf, which would have been the cheapest and more logical option. Instead it opted to renovate, in an attempt to appeal to the work force once more. Unfortunately, as is often the case, build costs always cost more than you think. In Citigroup’s case, £1.1bn more.

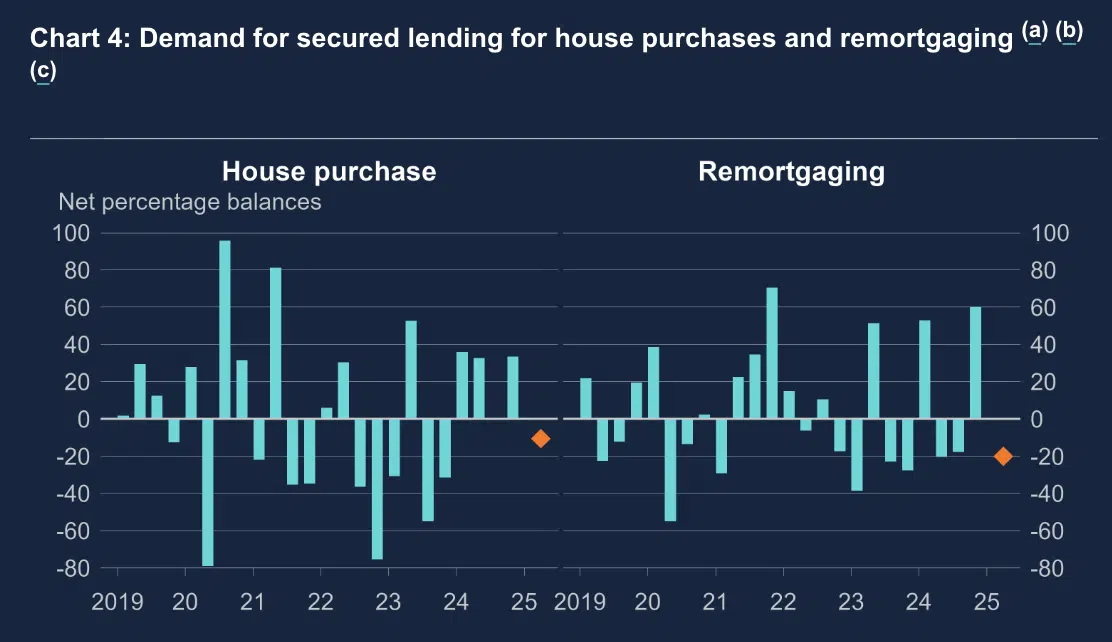

Bank of England Market Credit Conditions Survey

The Bank of England Market Credit Conditions Survey showed lending increased in Q4 of 2024 but is expected to dip again at the start of the year. Those looking to have a fighting chance of making the stamp duty deadline bought with time to spare while those looking at remortgaging, sick of speculation and yo-yoing rates locked in, for greater peace of mind.

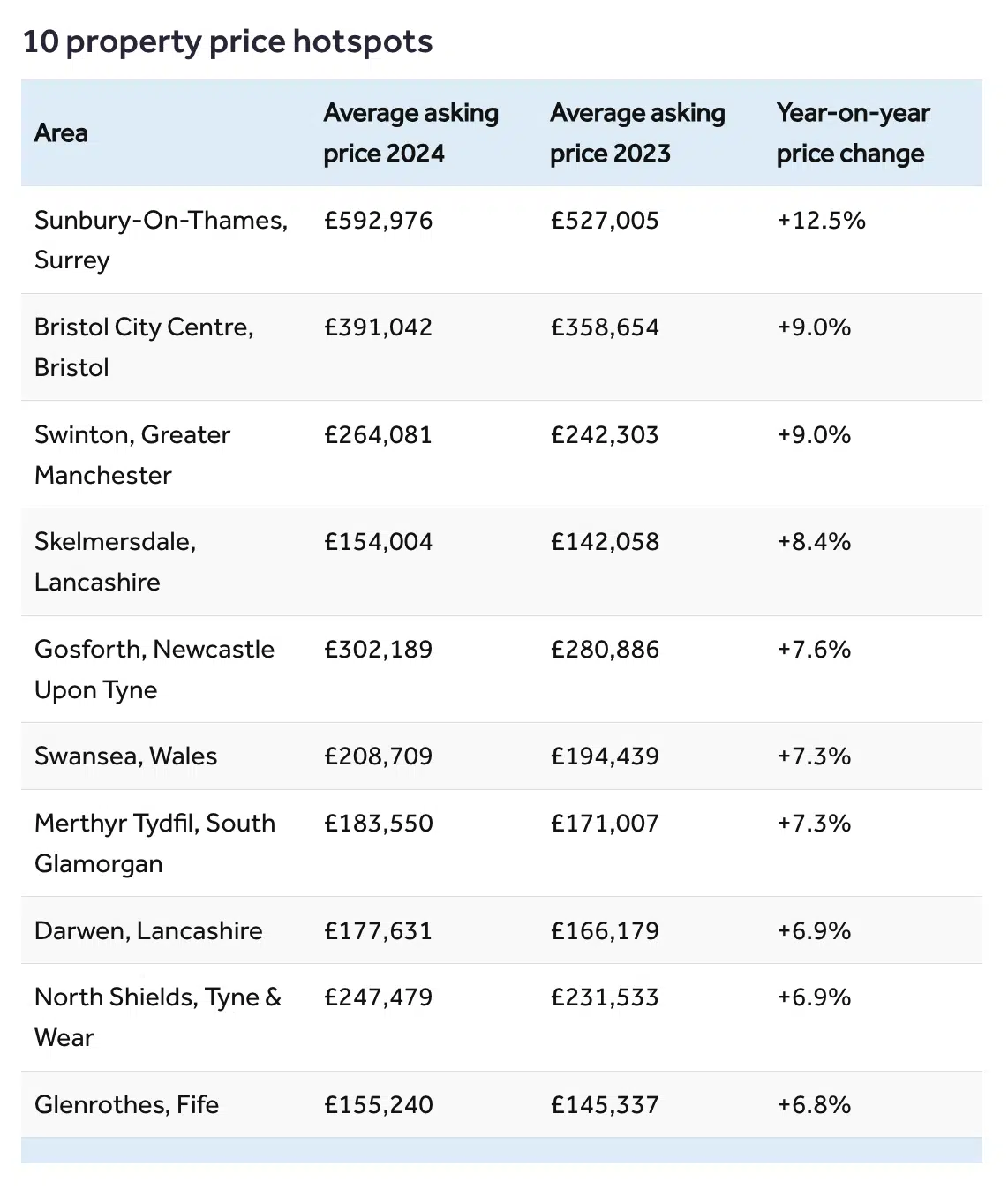

Rightmove’s top 10 asking price hot spots

According to property portal Rightmove, nationally, the average asking price tiptoed up from £355,177 in 2023, to £360,197 by the end of 2024. However all is not equal, and in pockets of the country asking prices rose. The largest increase was in Sunbury-On-Thames, on the outskirts of the Capital. Sellers here asked for 12.5% more than last year. Notice the areas where prices increased were in areas where prices are still appealing to first time buyers and are located close to city centres.

Amendments to the Renters’ Rights Bill

The third reading of the Renters’ Rights Bill was conducted in Parliament this week, bringing the bill another step closer to being realized. Below are some of the amendments made:

- Landlords can’t accept more than one month’s rent in advance in respect of a tenancy or licence of residential accommodation.

- Student tenancy agreements may not be signed before 1 March in the year in which the tenancy is intended to take effect.

- Duty placed on local authorities to help care leavers pay or guarantee any required deposit to enable them to agree a tenancy in the private rented sector.

- Tenants to pay rent to an independent individual responsible for investigating complaints made against members of a landlord redress scheme under section 62.” Only if they are satisfied will rent be paid to the landlord.

- Mediation provided for rent pauses for home adaptations

- Landlords must give permission for home adaptations for people who have disabilities where a Home Assessment has been carried out.

- Landlords fees will fund property ombudsman

- Guarantors aren’t liable to pay tenant fees should they die

- Restrictions on the requirement for tenants to provide a guarantor if the tenant has relevant funds and income to pay rent.

- The sum for which the guarantor may become liable under the relevant guarantee shall not exceed a sum equal to six months’ rent.

- Requirement on landlords to pay for alternative accommodation if the property is uninhabitable.

- Landlord shall not be entitled to increase the rent during a fixed period

- The limits would be calculated by reference to increases in CPI or median national earnings.so that when determining rents tribunals must take into account the limits on rent increases and need not consider existing market rates.

- Rents can’t be adjusted upwards just because landlord does energy efficient upgrades

- Landlord and dwelling entries to be registered on a Private Rented Sector Database which will be fee based.

- A registered social landlord can take possession where a tenant has been provided with alternative accommodation while redevelopment affecting the tenant’s original home is carried out.

The To Do List:

- Assessment of operation of possession process

- Assessment of appropriate insurance products are available to landlords to protect landlords from tenants on benefits or with pets

- Short term lets to be reviewed within two years of the passing of this Act.

- Review of tenancy deposit schemes and requirements which must consider tenancy “passporting”; and measures to improve trust in the deposit dispute process.

Mortgage rules could be broken to enable growth

Reeves’ master plan for growth has been scuppered by stubborn inflation, leaving interest rates higher than hoped. As a result, she is galvanizing financial regulators to allow lenders to open their books to more buyers with smaller deposits (currently only 15% of their order book) and to relax affordability rules (currently set at 4.5 times the buyer’s annual salary). This requirement could be scaled back, and previous rental payment history could be considered. This would enable more buyers to get on the property ladder and provide those moving up with an additional leg up. It would also help support prices and encourage builders to construct more homes. The concern is that what is considered “responsible” risk may unintentionally lead to profiteering, putting buyers at greater long-term risk.

And that concludes another UK Property News Recap – 17.01.2025. If you have any comments or suggestions, please get in touch.