This week demand, profits and confidence dropped, service charges soared and house prices stagnated. Lenders finally pulled their finger out and started competing for business, post base rate cut, which in turn will boost sales and developer optimism but first time buyers may have to wait till later in the year before they can feel the same benefit. Welcome to another UK Property News Recap – 14.02.2025

UK Government’s Housing Initiatives

Labour started the week by doubling down on their commitment to build 1.5m homes and announced a coalition of government with HM Land Registry and experts from the Digital PropertyMarket Steering Group – on a 12-week project to decide on the design and implementation of agreed rules on data so that “moving forward” it will be easier to share information between conveyancers, lenders and other parties involved in a transaction.

In addition, Angela Rayner plans to crack down on exploitative landlords with a new licensing scheme, tougher standards and the ability to stop housing benefits going to rogue and criminally supported housing landlords.

Leasehold services charges jump 11%

The rise in services, insurance, and utility prices has been reflected in service charges, causing the typical bill to increase by 11% last year, reaching £2,300 annually, or £192 per month. This average spike is partly due to the growth of new developments in the north, which come with expensive facilities to run and maintain. The upcoming Leasehold and Freehold Reform Bill, expected to become law by the end of the year, will provide clarity on quotes and eliminate insurance commissions, preventing leaseholders from being overcharged and helping to contain service charges, making properties more attractive to future buyers.

Knight Frank Housebuilder survey reports gloomy outlook

Almost a third of the developers in Knight Frank’s housebuilder survey said “weak demand for their affordable units, alongside a gloomy economic outlook, will have the greatest impact on housebuilding this quarter.” In other words…if you can’t afford to borrow you can’t afford to build or buy….Housing associations have a cladding and remedial TO DO list longer than their arm, with little money to cover this, so further investment – however much wanted – isn’t possible for the time being.

Interest rate change divided

The base rate may have dropped last week but average interest rates didn’t shift till Wednesday. The average 2-year and 5-year fixed residential mortgage rates, according to Moneyfacts, showed the average 2-year fixed shuffle down from 5.49% to 5.45% and the average 5-year fixed from 5.30% to 5.26% on the previous working day. However for those with a 40% deposit Santander was once again first out of the gates, offering fixed residential rate deals at 3.99% lasting for two and five years. Keen not to miss out, Barclays, TSB and Lloyds followed suit. Great news for some but little help to others struggling to cobble together a deposit.

No “mothing” around

A multi-billionaire won her court case to return her moth-infested £32.5 million Notting Hill mansion after the seller was less than truthful in his property information forms and enquiries. His defense was full of holes; he argued that moths were not considered vermin and therefore did not disclose their presence.

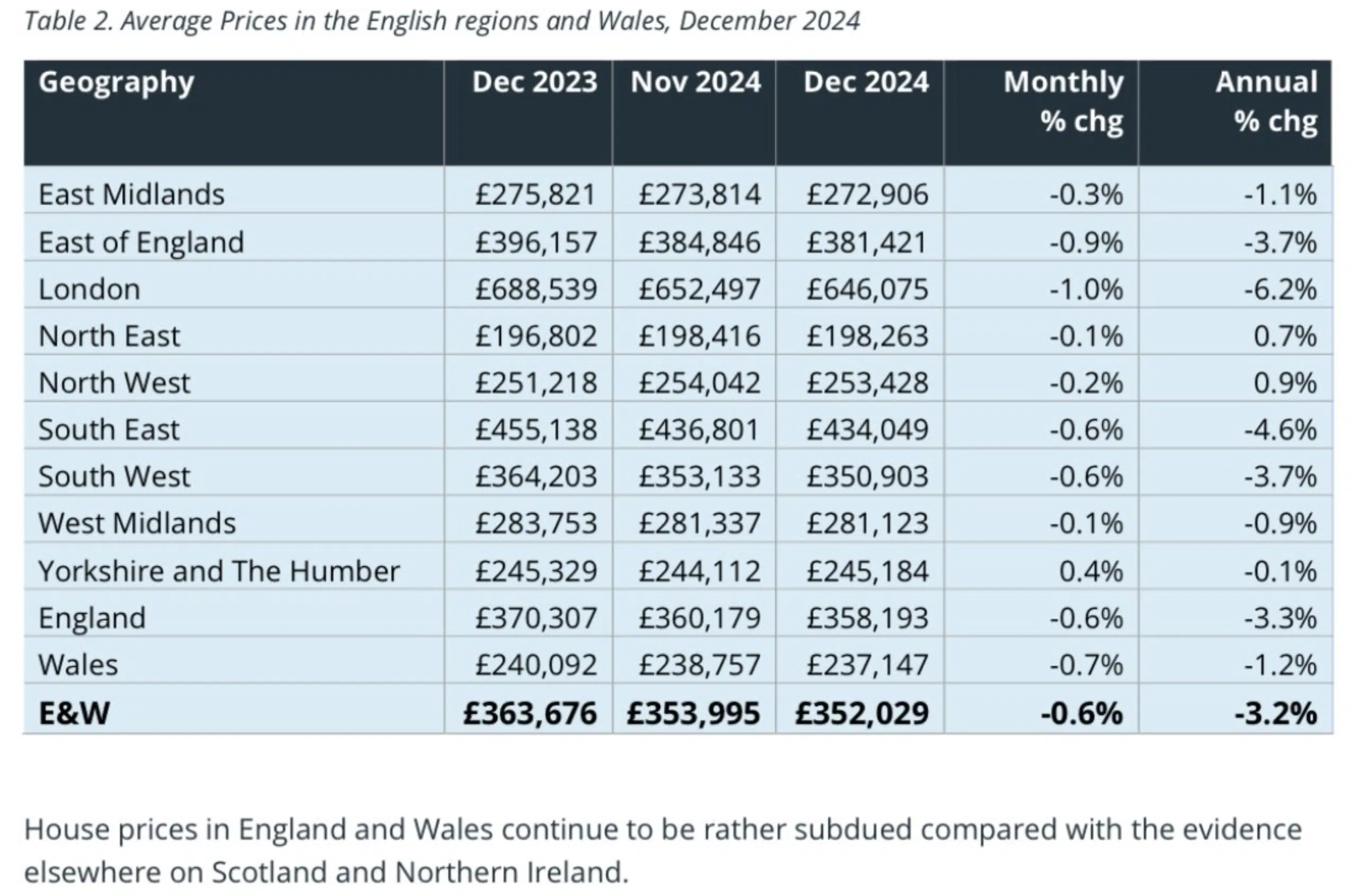

Acadata HPI shows price growth remains stunted

According to Acadata average house prices in England and Wales increased by 0.1% in the month of January but annual rates remain on ice. Moving forward prices are expected to show some growth dependent on “rate” conditions.

Bellway p.l.c. hopes to have turned a more profitable corner

In Bellway PLC’s trading update for the six months ending 31 January 2025, completions rose by 11.9%, and the group’s average selling price edged up to £310,600, from £309,278. At the same time, their forward order book grew from 3,970 to 4,726 homes, with volume output expected to reach at least 8,500 homes for the full year, compared to 7,654 in 2024.

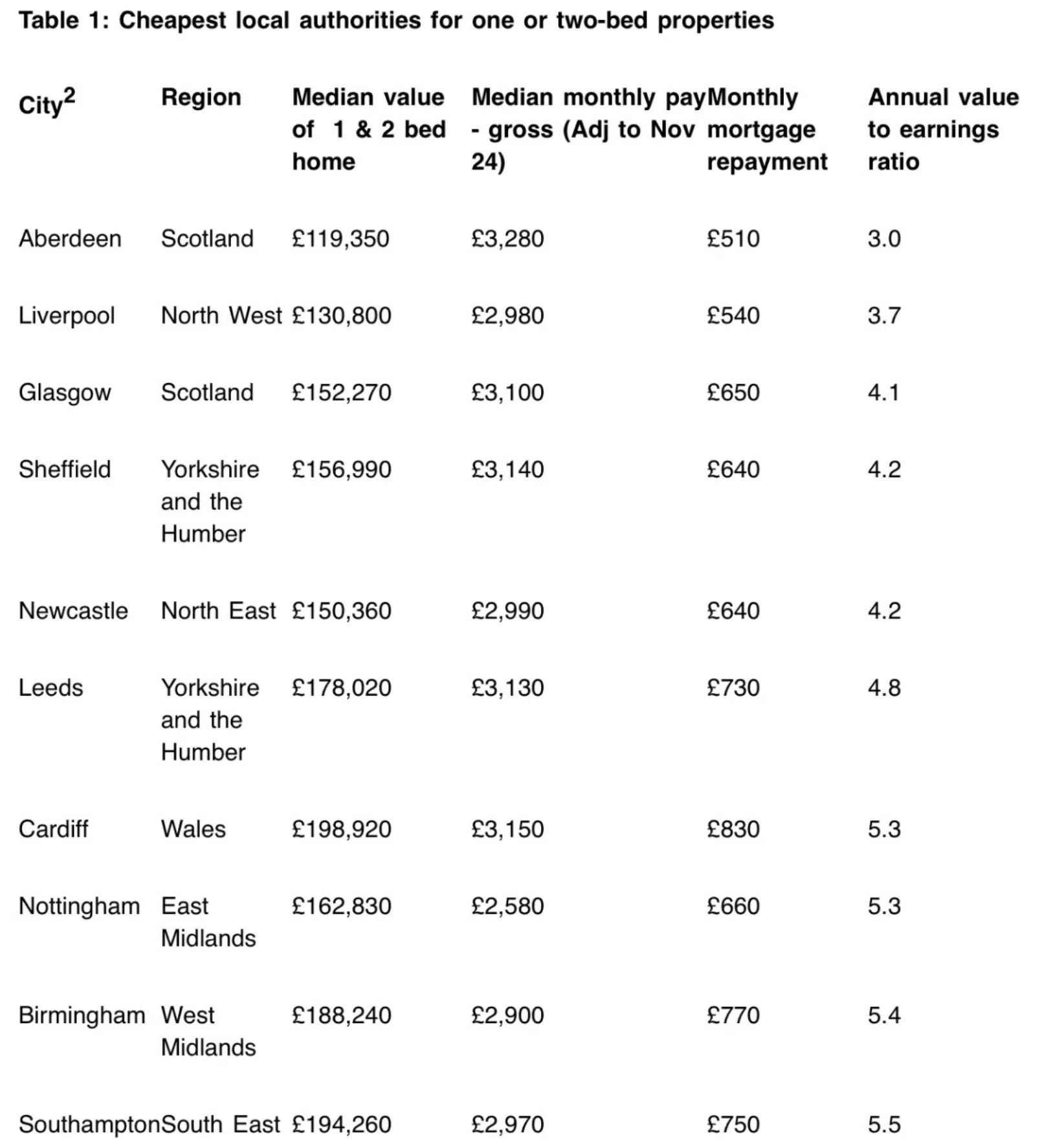

The most affordable UK Cities for singletons to buy

Property portal Zoopla reveals the most affordable UK city for singletons to buy was Aberdeen. In England, Liverpool and in the Capital, Havering. For those wedded to the south, the areas with the greatest improvement in affordability, as a result of stagnating growth and increased wages, were Bristol, Oxford, Portsmouth and Cambridge. Despite this mortgage repayments remain significantly higher than in southern regions.

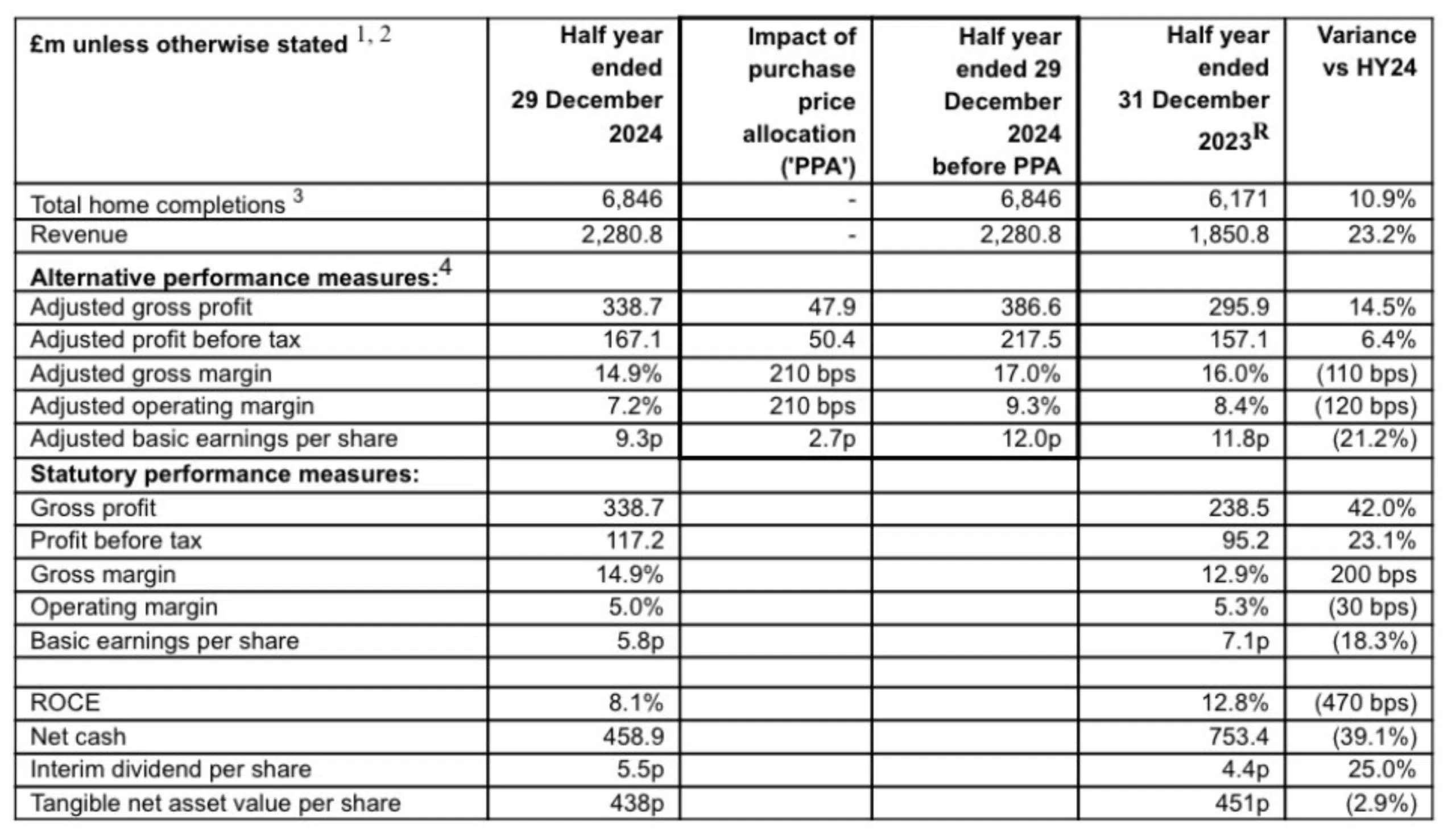

Barratt Redrow look to the future

Barratt Redrow half year results for the period ended 29 December 2024 showed operating margins squeezed but completions and revenue, overall, remaining consistent. Moving forward the group expects to deliver c. 22,000 homes per annum in the medium term, and their operating margin to “spring” back, “to c. 15% and return on capital employed (including land creditors) to c. 20%.”

Tenants peeked outside at the rental market and opted to stay put in increasing numbers

The DPS found that only 777,000 deposits were registered by landlords in 2023-4, a 70% drop when compared to eight years ago. At the same time, the average tenancy increased to 910 days. Tenants, preferring the landlord they know versus the landlord they don’t, charging more.

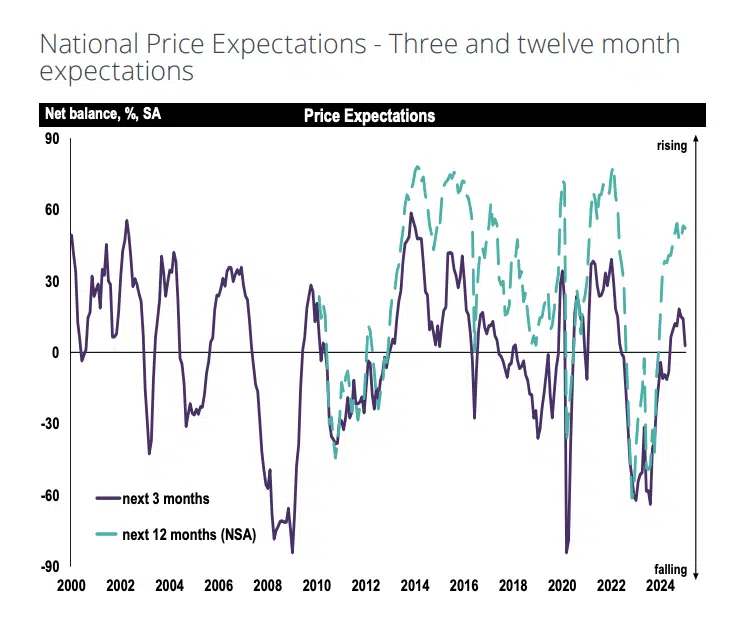

RICS: Residential Market Survey – January 2025

Overall, the UK property market appeared to stagnate in January, with the New Year rate sale falling flat and first-time buyers realizing that meeting the stamp duty deadline was unlikely. Meanwhile, more properties hit the online portal shelves and valuations rose as sellers prepared for the spring season.

Prices surged in the North and North West, while the rest of the country saw more modest increases. According to the RICS Residential Market Survey, respondents expect prices to stabilize in the short term before gaining momentum later in the year, especially if further rate cuts occur.

In the lettings market, demand continued to wane but landlord instructions also fell. As a result rental prices stagnated but are also expected to also pick up as the year progresses.

ONS: Construction output

Construction output showed a slight increase in 2024, rising by 0.4% over the year and 0.5% in the final quarter, according to the ONS. However, December’s winter weather and the festive season caused disruptions, leading to a decline in output across five of the nine sectors. The biggest drops came from non-housing and private housing repair and maintenance, which fell by 1.8% and 1.4%, respectively. This contrasted with overall annual growth, which was driven by repair and maintenance, while new work saw a decline.

12 new UK towns will be decided upon come summer

Keir Starmer attempted to update the public on new housing sites that will be identified to form 12 new UK towns each with the capacity for at least 10,000 homes, along with the necessary infrastructure, but protesting farmers drowned him out with the sound of their horns. The new towns are due to be identified by summer and will be managed by regional development corporations, which will receive an initial injection of public funding to purchase land. This investment will be recouped once the land is sold to private developers at a higher value, with the proceeds helping to cover the cost of infrastructure.

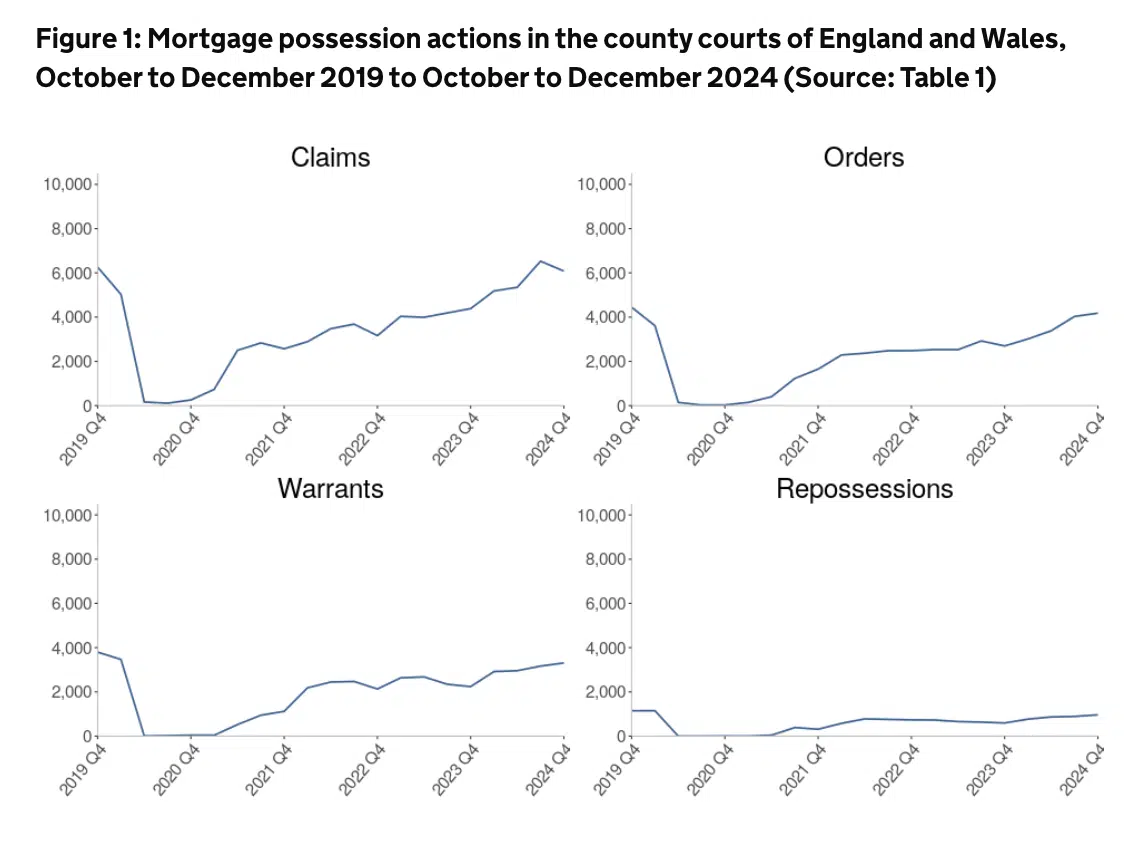

Landlord and mortgage possessions rise in Q4 2024

The latest mortgage and possession data for Q4 2024 reveals significant increases across several key areas. Mortgage possession claims rose by 39%, from 4,385 to 6,080, while possession orders jumped by 55%, from 2,697 to 4,178. Warrants saw a 48% increase, climbing from 2,240 to 3,305, and repossessions by county court bailiffs rose by 61%, from 595 to 957.

The rise in landlord possession claims was primarily driven by London but was partially offset by decreases in Wales, the North East, and the South West. This resulted in a modest overall increase of 3%, bringing the total to 24,010 claims.

First time buyers increase in 2024 by 20%

According to lender Halifax, 54% of all property purchases involving a mortgage were first time buyers in 2024, a 20% increase on 2023 levels. To achieve this two thirds of these cosied up to buy, and waved a curt goodbye to the rental market.

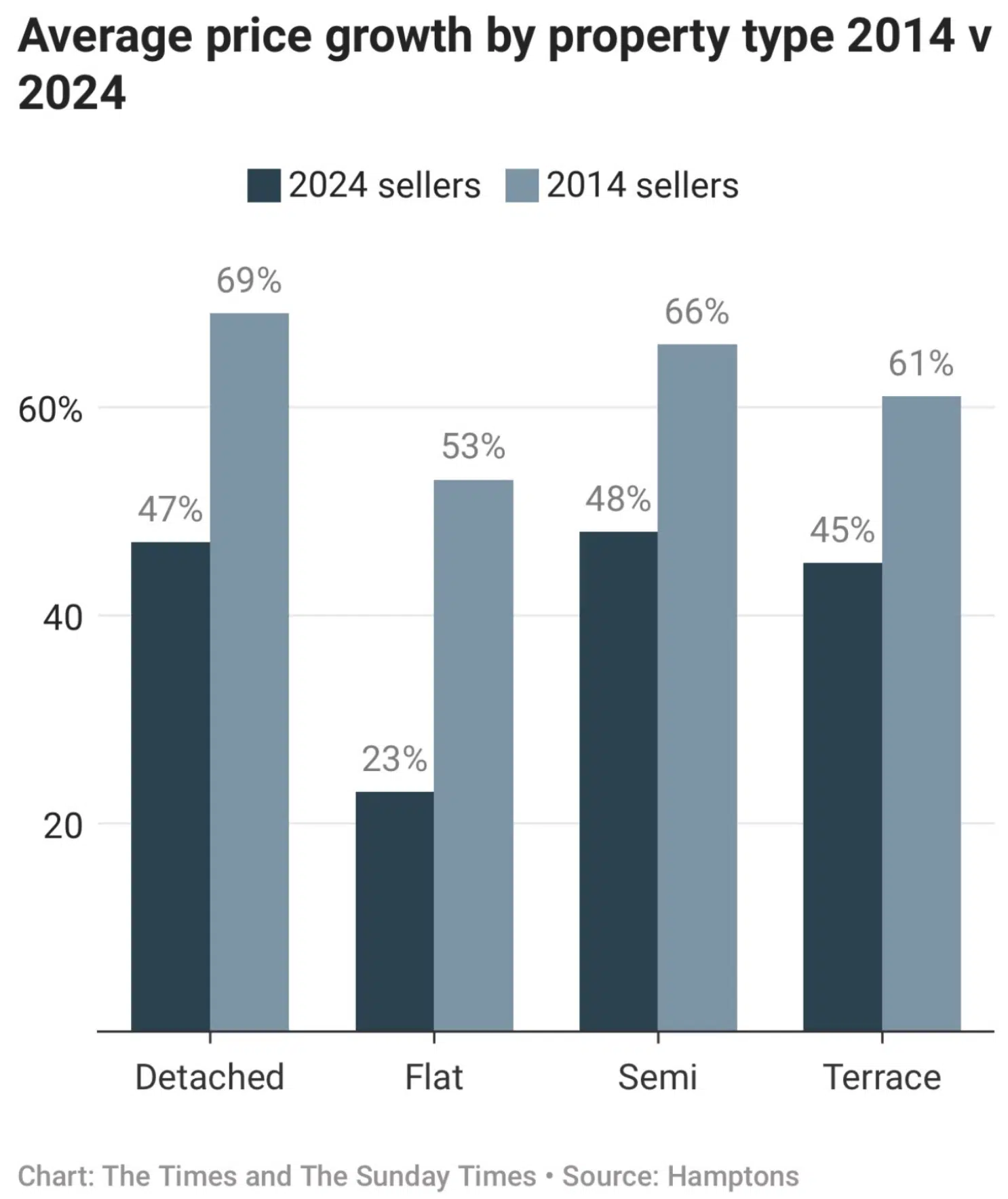

House values rise twice as fast as flats

The estate agency Hamptons, found the typical seller who sold their house in 2024 got 31% more than what they bought it for five years ago, but it took the average flat owner ten years to see a 30% increase in value. Increases in services charges, insurance and cladding issues have tainted the flat market reducing any uplift in value.

And that concludes another UK Property News Recap – 14.02.2025. If you have any comments or suggestions, please get in touch.